Title First Agency works hard to ensure a seamless experience for Realtors and their clients. From contract to closing, Title First handles all the details to help your transactions run smoothly and close on time.

Title First Agency can help Realtors by getting the names, addresses and phone numbers for properties that their client are interested in buying. Maybe the buyer wants to find a home of a certain age or in a particular area – whatever it may be, a Title First Agent has the ability to access a lot of data and can find the information needed. Buyers often drive around neighborhoods that they want to live in and see the perfect home for their family. A Title First Agent can look up the information of who owns the home and how long they have been there at the exact address. This will enable the Realtor and the buyer to put together a homebuyers letter to owner.

Title First can assist Realtors in promoting their business with our full line of marketing solutions. For your next listing, make a good first impression on potential clients and prospective buyers with a bound presentation of property information. We have the ability to help you design, print and mail your full-color glossy, postcards. Use our Net-to-Seller tool that will help estimate a client’s profit and present it in a professional format to be shared. Or, give our Title First Agent App a try to provide a higher level of service to your clients. This app will enable you to give quick and easy estimates to any real estate financial question. The app features net sheets, quick estimates, closing,costs, prorated taxes and much more. Finally, email us your MLS link, logo and personal photo and let us create a professional full-color info sheet for your listing.

Title First Agency has experienced real estate lawyers who have worked many years through settlements and closings. It’s an invaluable asset to always have legal experts on hand with a good title company. The buyer, seller and you, the Realtor, can have peace of mind that purchases and end-to-end processes of closing on a property are performed seamlessly and on time.

The Bottom Line: At Title First Agency, we measure our success by your success. That’s why we offer a variety of services to help you growyour real estate business. Beyond the above listed services, the issuing of insurance, and performing title searches, we can manage the escrow account for the home sale. We safeguard all money and documents related to the transaction for the parties involved, such as the deed to the home, closing costs, earnest money deposit and the down payment.

When buying a new home, you’ll quickly hear all sorts of terms tossed into conversations. Most people tend to assume that Property Deeds and titles are the same, but in reality refer to two separate legal concepts. When you own a property entirely, you will possess both the Deed and title. But a title is distinct from a Deed. Mixing the two up can cause problems if you don’t know what you’re using.

Deeds are simply the legal documents that transfer title from one entity to another, not titles themselves. They must be written documents, according to the Statute of Frauds. Another term for “deed” is “vehicle of the property interest transfer.” In most states, deeds are required to be recorded in a courthouse or an assessor’s office to make them fully binding, but a failure to file them does not change the transfer of title. It just means that the deed is not “perfected.” An imperfect deed does not mean that there is a problem with the title. It’s just a problem with the way that the paperwork surrounding the deed was handled.

A Title is a legal way of saying you own a right to something. When buying a home, the title refers to ownership of the property, and you have the rights to use that property. It may be a partial interest in the property or it may be full. However, because you have a title, you can access the land and potentially modify it as you see fit. A Title also means that you can transfer that interest or portion that you own to others.

The Bottom Line: Deeds and certificates of title have one function in common: both provide proof of ownership of property. The certificate of title must contain enough information to identify the piece of property and any encumbrances, such as mortgages. The deed to a piece of property may also include conditions of ownership and more extensive information about the property. The deed itself is also an integral part of a real estate transfer.

Title companies offer one of the most important types of insurance that one can buy. For most people, a residence or commercial property may be the most expensive asset they own. Title insurance in a real estate transaction has great value to the average consumer.

Think about it this way, what is the first thing you do when you go buy a car? You probably (hopefully!) pick up the phone and call your insurance agent to insure the vehicle. So naturally, insuring your real estate would be more pressing, since the value of it can be quite substantial.

So what should a good title company offer? Since the Ohio Department of Insurance regulates title insurance in the state of Ohio, and the Ohio Title Insurance Rating Bureau dictates all premiums, a title company can set itself apart by the customer service they offer along with the partner networks they share. Working with a large title company that does business on a national level has many advantages.

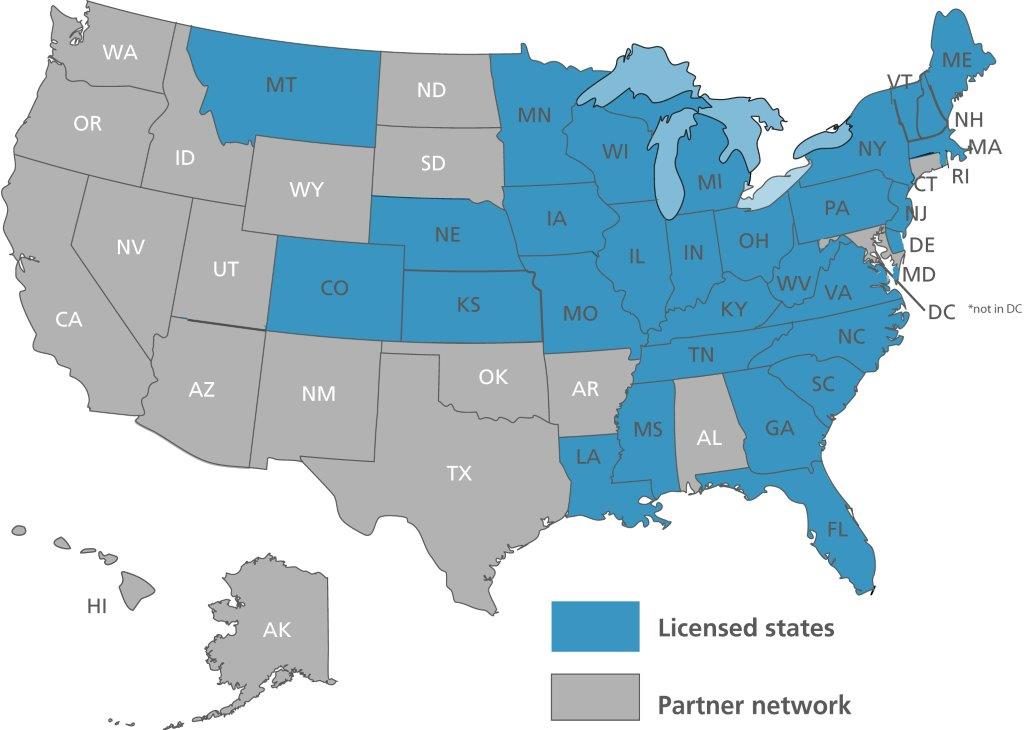

Title companies with the ability to write on multiple underwriter paper have the ability to provide more options and flexibility to their clients. For instance, Title First Agency is licensed in 33 states and can conduct business in all 50 states through its partner network and affiliations. Title First utilizes five of the leading title insurance underwriters in the business to issue title insurance policies to end consumers. (Check them out at https://titlefirst.com/underwriters/) This benefits the consumer in many ways, especially when a potential title issue arises and one underwriter is willing to take the risk while another may not be so willing.

Another benefit of a national title company is the increased level of protection of private information of both clients and consumers. There is a vast amount of private information necessary in conducting a real estate transaction. Some title companies have specific protocols as well as various checks and balances in place to ensure consumer privacy, which is paramount in today’s world. At Title First, we pride ourselves on achieving the highest certification for cyber security audits, without exception, known as SSAE 18. In addition, Title First is Best Practices Certified by the American Land Title Association. In order to obtain these certifications, Title First has participated in rigorous, outside, third party audits that test our systems and ensures the company maintains privacy at every level. What does this mean for you and your clients? It means that you can rest easy knowing your client’s information and financials are safe within our company.

Larger, national title companies, such as Title First, have a strong network of contacts in the real estate industry. Whether it be lenders, national vendors, realtors, or private attorneys – national title companies have access to all of these partners and more, which provides consumers and clients with access to any resources they may need during their transaction. This access creates the best overall experience at the closing table for the consumer and their realtors! Some lenders will only work with certain title companies – some have a “preferred vendors” list. Title First has built these affiliations and relationships over more than 60 years in the business. A trusted partner can provide you with peace of mind so you can make it to your next listing appointment or showing, on time and without a worry.

Why not use a company with a proven history, and a large network of providers to ensure you get the most for your client? Title First does just that – “National Reach, Local Touch” – at every step of the way.

Title insurance. What would happen if you didn’t have it? What if you decided it’s not worth it? For starters, you would have bought a home that you can’t prove you bought legally. The title is the your right to possess and use the property .

What can happen without it? Problems arise when there are parties who want to be repaid loans and bills collateralized by the same property. There is the lender that made the first mortgage; the lender that opened the home equity line of credit; contractors whose unpaid bills resulted in liens on the property; taxing districts; and even homeowners’ associations waiting to be repaid from the proceeds of the house. Who will get paid and when? Without a title to the home? You are on the hook for the bills.

Title First will do a title search so that you don’t end up buying all those problems with the house. Being the new owner doesn’t mean that the problems go away. If you don’t have title insurance, you might have to sell the house just to repay the outstanding bills which have become yours.

A title search is usually required by all lenders. They want to make sure that title problems are cleared up before you buy the house. If the lender makes a mortgage with the home as collateral and it already has claims against it, the lender will lose money.

During the process of buying a home, Title First will check the property’s ownership history. Ideally, there is a “clear title”, meaning the current owner, who is selling to you, has a complete ownership stake in the property, without any legal claims against it.

If Title First does not find any outstanding claims or title defects, know that there could be a “yet to be discovered” issue that could arise and sully the ownership of the property years after the purchase. Maybe there was a mistake in the ownership history, an oversight committed by the title researcher, even a previously unknown heir. There could be a possible pending lawsuit or legal judgment.

A title defect that arises after a loan closing could, at the very least, mean a variety of legal costs — and, in a worst-case event, the loss of your property and the money you’ve put in it.

The Bottom Line:Title First works hard to ensure a seamless experience for you and your clients. From contract to closing, Title First handles all the details to help your transactions run smoothly and close on time.

The reasons for getting title insurance are not obvious at first. One thing we stress at Title First is the importance of owner’s title insurance policies for real estate transactions. When buying a home, a foreclosed property or a short sale, an owner’s title policy is necessary.

Title insurance helps to safeguard that there are not any legal claims out there against the home you want to buy in a short sale. Usually, the owner can’t afford mortgage payments anymore, so the risk is that there are also liens for other debts such as overdue taxes, unpaid contractors’ bills, etc. More often than not, short sales include unsatisfied obligations and if you are to close on the home with these unsettled claims, you would be held responsible for the outstanding debt. require the title insurer to deal with the seller and lien holders on your behalf;

When you have Title First helping, we can require the seller to take care of the outstanding problems prior to the closing, deal with the lien holders directly, and even ask the seller to lower the price of the house. Without a title policy, you may end up with multiple problems.

What Title First will look for is not only unsettled claims but also for fraud, forgery, clerical errors, omissions, encroachment issues, restrictions, judgments, divorce decrees, missing heirs and other problems that are sometimes impossible to anticipate. Having an owner’s policy ensures that Title First will stand behind you, should a problem occur down the road.

Dedicated to innovation and passionate about service, Title First Agency is your comprehensive, nationwide resource for title and real estate settlement services.

To better serve its customers, Title First has implemented best practices and third-party audits, equipping itself to facilitate compliance efforts. In 2014, Title First instituted ALTA Best Practices and continually reviews its compliance. More importantly, in 2015, Title First completed its examination in conformity with Statement on Standards for Attestation Engagements (SSAE) No. 16 through an independent third-party auditor. Each year, Title First continues its SSAE examination, and in 2017 earned the SSAE-18 certification. Title First is one of the few title agencies in the industry having an SSAE-18 certification.

In fact, Title First is one of only two title companies in the state of Ohio to earn the SSAE certification. This certification provides reassurance that Title First Agency is in compliance when it comes to financial controls and internal procedures for data security, availability, processing integrity and privacy.

Before you buy a new house, a qualified home inspector is always your best bet for a thorough home evaluation, but you should also have a general understanding of what to look out for. A bad home inspection has the potential to derail a real estate transaction, especially if what’s uncovered is an expensive problem. Here are four issues that have been deal breakers, according to some Realtors.

Faulty Electrical Wiring: The electrical system is an important, and potentially hazardous, part of a home, which is why it is included in every thorough home inspection Newer homes have more supply of power and electrical outlets. Older homes do not. A good inspector should check the outlets throughout the home as well as check the interior of the electrical breaker/fuse box assuring that there are no “double taps” – two electrical circuits attached to a single breaker – as it is a fire hazard. The wires, conduits, and boxes should be securely fixed to the building. There should be no visible signs of damage or deterioration. There should be at least one ground rod or other approved grounding means present at the service.

Plumbing: Some of these issues are obvious. Skilled inspectors are trained to find obvious, like a clogged toilet as well as the not so obvious, like illegal pipes that could result in being cited for plumbing violations. He will look around the entire home for signs of mildew, fungus or mold related to water leaking from broken pipes and cracks in the ceiling or floor.

Grading Toward the Home: Water in the basement, damp or wet crawlspaces, foundation movement, cracking and settlement may all be caused by grading. Water in the foundation could lead to rot in the walls, framing members and mold. Some indications of foundation movement include windows that are out of square; interior doors that have large, uneven gaps at the top when the door is closed; or floors visibly out of level. Some of the most experienced home inspectors believe that the most common issue they find during inspections is the lack of grading (improperly sloped soil) away from the home.

Roofing: A roof usually lasts about 30 years, so you will need to find out when it was installed. A home inspector will look at the quality of the shingles and know if any are curled, broken, or even missing which are signs that you might need a new roof soon.

The Bottom Line: Whether any of these issues are deal breaker depends on your preferences and needs. Any issue such as the four listed might be too expensive or time-consuming to fix. However, you might find these issues acceptable and have the resources to get them fixed. The home inspector should not tell anyone to buy or not to buy a home. It’s just his job to provide all the information needed so that the home buyer can make the right decision for them.

Having title insurance from Title First Agency will protect you from the possibility of a claim to ownership of your home by someone. It’s hard to believe this can happen, but it is more common than people think. It’s not usually a plot to steal your home but a confusion with the deed. The laws regarding property ownership are complex and when liens come into play, someone may believe they still own a house that was technically taken over by a bank.

Title problems appear when parties want to be repaid loans and bills outstanding by the same property. There is a lender that made the first mortgage; the lender that opened the home equity line of credit; contractors whose unpaid bills resulted in liens on the property; taxing districts; and even homeowners’ associations all lining up to be repaid from the proceeds of the house, it’s easy to see how they might not agree on who gets paid what, and when.

Without a title search, the buyer buys all those problems along with the house. The problems don’t go away just because there is a new owner. There have been examples of homeowners having to sell the house just to pay the bills.

Title searches are required by all lenders to be sure that title problems are cleared up before a home is bought. It’s not for you. It’s for them. If the lender makes a mortgage with another that already has claims against it, that lender is going to lose that money.

The Bottom Line: The title is proof that a piece of property is legally owned. It’s an extremely important document. Without a clear title, you are taking a tremendous gamble in purchasing a house or other property. The experts at Title First Agency oversee and perform thousands of closings each year. When using Title First, you can sign confidently on the dotted line knowing that all the details of your title transfer and closing are in proper order. We are here to answer any questions you may have about buying or selling a home, and our team will guide you through the entire process.

Appraisal management company (AMC): An institution operated independently of a lender that, once notified by a lender, orders a home appraisal. Appraisal: An informed, impartial and well-documented opinion of the value of a home, prepared by a licensed and certifed appraiser and based on data about comparable homes in the area as well as the appraiser’s own walk-through. Approved for short sale: A term that indicates that a homeowner’s bank has approved a reduced list price on a home and the home is ready for resale. American Society of Home Inspectors (ASHI): A not-for-profit professional association that sets and promotes standards for property inspections and provides educational opportunities to its members. (i.e., Look for this accreditation or something similar when shopping for a home inspector.)

Attorney state: A state in which a real estate attorney is responsible for closing. Back-end ratio: One of two debt-to-income ratios that a lender analyzes to determine a borrower’s eligibility for a home loan. The ratio compares the borrower’s monthly debt payments (proposed housing expenses, plus student loan, car payment, credit card debt, maintenance or child support and installment loans) to gross income. Buyer’s market: Market conditions that exist when homes for sale outnumber buyers. Homes sit on the market a long time and prices drop. Meaning = you win. Cancellation of escrow: A situation in which a buyer backs out of a home purchase. Capacity: The amount of money a home buyer can afford to borrow. Cash-value policy: A homeowners insurance policy that pays the replacement cost of a home, minus depreciation, should damage occur. Closing: A meeting during which ownership of a home is transferred from seller to buyer. The closing is usually attended by the buyer, the seller, both real estate agents and the lender. Closing costs: Fees associated with the purchase of a home that are due at the end of the sales transaction. Fees may include the appraisal, the home inspection, a title search, a pest inspection and more. Buyers should budget for an amount that is 1 to 3 percent of the home’s purchase price. Closing Disclosure (CD): A five-page document sent to the buyer three days before closing. This document spells out all the terms of the loan: the amount, the interest rate, the monthly payment, mortgage insurance, the monthly escrow amount and all closing costs. Closing escrow: The final and official transfer of property from seller to buyer and delivery of appropriate paperwork to each party. Closing of escrow is the responsibility of the escrow agent. Comparative Market Analysis (CMA): An in-depth analysis, prepared by a real estate agent, that determines the estimated value of a home based on recently sold homes of similar condition, size, features and age that are located in the same area. Compliance agreement: A document signed by the buyer at closing, in which he or she agrees to cooperate if the lender needs to fix any mistakes in the loan documents. Comps: Or comparable sales, are homes in a given area that have sold within the past six months that a real estate agent uses to determine a home’s value. Condo insurance: Homeowners insurance that covers personal property and the interior of a condo unit should damage occur. Contingencies: Conditions written into a home purchase contract that protects the buyer should any issues arise with financing, the home inspection or other. Conventional 97: A home loan that requires a down payment equivalent to 3 percent of the home’s purchase price. Private mortgage insurance, which is required, can be canceled when the owner reaches 80 percent equity. Conventional loan: A home loan not guaranteed by a government agency, such as FHA or the VA. Days On Market (DOM): The number of days a property listing is considered active. Depository institutions: Banks, savings and loans and credit unions. These institutions underwrite as well as set home loan pricing in-house. Down payment: A certain portion of the home’s purchase price that a buyer must pay. A minimum requirement is often dictated by the loan type. Debt-to-income ratio (DTI): A ratio that compares a home buyer’s expenses to gross income. Earnest money: A “security deposit” made by the buyer to assure the seller of his or her intent to purchase. Equity: A percentage of the home’s value owned by the homeowner. Escrow account: An account required by a lender and funded by a buyer’s mortgage payment to pay the buyer’s homeowners insurance and property taxes. Escrow agent: A neutral third-party officer who holds all paperwork and funding in trust until all parties in the transaction fulfill their obligations as part of the transfer of property ownership. Escrow state: A state in which an escrow agent is responsible for closing. Fannie Mae: A government-sponsored enterprise chartered in 1938 to help ensure a reliable and affordable supply of mortgage funds throughout the country. Federal Reserve: The central bank of the United States, established in 1913 to provide the nation with a safer, more flexible and more stable monetary and financial system. Federal Housing Administration (FHA): A government agency created by the National Housing Act of 1934 that insures loans made by private lenders. FHA 203(k): A rehabilitation loan backed by the federal government that permits home buyers to finance money into a mortgage to repair, improve or upgrade a home. Foreclosure: A property repossessed by a bank when the owner fails to make mortgage payments. Freddie Mac: A government agency chartered by Congress in 1970 to provide a constant source of mortgage funding for the nation’s housing markets. Funding fee: A fee that protects the lender from loss and also funds the loan program itself. Examples include the VA Funding Fee and the FHA funding fee. Gentrification: The process of rehabilitation and renewal that occurs in an urban area as the demographic changes. Rents and property values increase, culture changes and lower-income residents are often displaced. Guaranteed replacement coverage: Homeowners insurance that covers what it would cost to replace property based on today’s prices, not the original purchase price, should damage occur. Homeowner Association (HOA): The governing body of a housing development, condo or townhome complex that sets rules and regulations and charges dues and special assessments that are used to maintain common areas and cover unexpected expenses respectively. Home equity line of credit (HELOC): A revolving line of credit with an adjustable interest rate. Like a credit card, this line of credit has a limit. There is a specified time during which money can be drawn; payment in full is due at the end of the draw period. Home equity loan: A lump-sum loan that allows the homeowner to use the equity in his or her home as collateral. The loan places a lien against the property and reduces home equity. Home inspection: A non-destructive visual look at the systems in a building. Inspection occurs when the home is under contract or in escrow. Homeowners insurance: A policy that protects the structure of the home, its contents, injury to others and living expenses should damage occur. Housing ratio: One of two debt-to-income ratios that a lender analyzes to determine a borrower’s eligibility for a home loan. The ratio compares total housing cost (principal, homeowners insurance, taxes and private mortgage insurance) to gross income. In escrow: A period of time (30 days or longer) after a buyer has made an offer on a home and a seller has accepted. During this time, the home is inspected and appraised and the title searched for liens, etc. Jumbo loan: A loan amount that exceeds the Fannie Mae/Freddie Mac limit, which is generally $425,100 in most parts of the United States. List price: The price of a home, as set by the seller. Loan estimate: A three-page document that is sent to an applicant three days after he or she applies for a home loan. The document includes loan terms, monthly payment and closing costs. Loan-to-value ratio (LTV): The amount of the loan divided by the price of the house. Lenders reward lower LTV ratios. Market value coverage: Homeowners insurance that covers the amount the home would go for on the market, not the cost to repair, should damage occur. Mechanic’s lien: A hold against a property, filed in the county recorder’s office by someone who’s done work on a home and not been paid. If the homeowner refuses to pay, the lien allows a foreclosure action. Mortgage broker: A licensed professional who works on behalf of the buyer to secure financing through a bank or other lending institution. Mortgage companies: Lenders who underwrite loans in-house and fund loans from a line of credit before selling them off to a loan buyer. Mortgage interest deduction: Mortgage interest paid in a year subtracted from annual gross salary. Mortgage interest rate: The price of borrowing money. The base rate is set by the Federal Reserve and then customized per borrower, based on credit score, down payment, property type and points the buyer pays to lower the rate. Multiple Listing Service (MSL): A database where real estate agents list properties for sale. Origination fee: A fee, charged by a broker or lender, to initiate and complete the home loan application process. Piggyback loan: A combination of loans bundled so as to avoid private mortgage Insurance. One loan covers 80 percent of the home’s value, another loan covers 10 to 15 percent of the home’s value and the buyer contributes the remainder. Principal, interest, property taxes and homeowners insurance (PITI): The components of a monthly mortgage payment. Private mortgage insurance (PMI): A fee charged to borrowers who make a down payment that is less than 20 percent of the home’s value. The fee, 0.3 percent to 1.5 percent of the yearly loan amount, can be canceled, in certain circumstances, when the borrower reaches 20 percent equity. Points: Prepaid interest owed at closing, with one point representing one percent of the loan. Paying points, which are tax deductible, will lower the monthly mortgage payment. Pre-approval: A thorough assessment of a borrower’s income, assets and other data to determine a loan amount he or she would qualify for. A real estate agent will request a pre-approval or pre-qualification letter before showing a buyer a home. Pre-qualification: A basic assessment of income, assets and credit score to determine what, if any, loan programs a borrower might qualify for. A real estate agent will request a pre-approval or pre-qualification letter before showing a buyer a home. Property tax exemption: A reduction in taxes based on specific criteria, such as installation of a renewable energy system or rehabilitation of a historic home. Round table closing: All parties (the buyer, the seller, the real estate agents and maybe the lender) meet at a specified time to sign paperwork, pay fees and finalize the transfer of homeownership. Seller’s market: Market conditions that exist when buyers outnumber homes for sale. Bidding wars are common. Short sale: The sale of a home by an owner who owes more on the home than it’s worth (i.e. “under water” or “upside down”). The owner’s bank must approve a lower list price before the home can be sold. Special assessment: A fee charged by a condo complex HOA when cash on reserve is not enough to cover unexpected expenses. Tax lien: The government’s legal claim against property when the homeowner neglects or fails to pay a tax debt. Third-party review required: Verbiage included in a home listing to indicate that the lender has not yet approved the home for short sale. The seller must submit the buyer’s offer to the lender for approval. Title insurance: Insurance that protects the buyer and lender should an individual or entity step forward with a claim that was attached to the property before the seller transferred legal ownership of the property or “title” to the buyer. Transfer stamps: The form in which transfer taxes are paid by the home buyer. Stamps can also serve as proof of transfer tax payment. Transfer taxes: Fees imposed by the state, county or municipality on transfer of title. Under contract: A period of time (30 days or longer) after a buyer has made an offer on a home and a seller has accepted. During this time, the home is inspected and appraised and the title searched for liens, etc. Under water or upside down: A situation in which a homeowner owes more for a property than it’s worth. Underwriting: A process a lender follows to assess a home loan applicant’s income, assets, credit etc. and the risk involved in offering the applicant a mortgage. VA home loan: A home loan partially guaranteed by the United States Department of Veteran Affairs and offered by private lenders, such as banks and mortgage companies. VantageScore: A credit scoring model relied upon by lenders to make lending decisions. A borrower’s score is based on bill-paying habits, debt balances, age and variety of credit accounts and number of inquiries on credit repots. Walk-through: A buyer’s final inspection of a home before closing. Water certificate: A document that certifies that a water account has been paid in full. The seller must produce this certificate at closing.

Closing a real estate deal, signing the papers to make a home yours, can be stressful and long and it involves many steps and procedural formalities. Many things must happen before you arrive at the closing. Here are a few important guidelines that need to happen between the moment your offer is accepted to the moment you get the keys to your new home.

Open an Escrow Agreement

An escrow account can be held by a neutral third party on behalf of the two principal parties involved in the transaction. They will hold all the money and documents related to the transaction until all is settled. A contract or escrow agreement is drafted, which the closing agent reviews for completeness and accuracy.

Title Search is Conducted and Title Insurance is Obtained

Once the title order is placed, the title company conducts a search of the public records. This should identify any issues with the title such as liens against the property, utility easements, and so on. If a problem is discovered, most often the title agency will take care of it without you even knowing about it. After the title search is complete, the title company can provide a title insurance policy.

There are two kinds of title insurance coverage: a Lender’s policy, which covers the lender for the amount of the mortgage loan; and an Owner’s policy, which covers the homebuyer for the amount of the purchase price. If you are obtaining a loan, the bank or lender will typically require that you purchase a Lender’s policy. However, it only protects the lender.

It is always recommended that you obtain an Owner’s policy to protect your investment. The party that pays for the Owner’s policy varies from state to state, so ask your settlement agent for guidance before closing.

Obtain a Closing Disclosure

Your lender must provide a Closing Disclosure to you at least three days prior to closing. Your lender may also have a closing agent provide the Closing Disclosure to you three days before you close your transaction.

If you or your lender makes significant changes between the time the Closing Disclosure form is given to you and the closing, you must be provided a new form and an additional three-business-day waiting period after receipt of the new form.

If the changes are less significant, they can be disclosed on a revised Closing Disclosure form provided to you at or before closing, without delaying the closing.

Be Ready to Close

As the closing day approaches, your agent will order any updated information that may be required. Once the agent has confirmed with the lender and the seller, a final date, time and location of the closing will be set.

On the day of the closing, all the work is complete. You are clear to close. A good Realtor will have been managing and making sure all the paperwork is done and getting the closing process prepared for you.

A fire destroys only the house and improvements. The ground is left. A defective title may take away not the only the house but also the land on which it stands. Title insurance protects you (as specified in the policy) against such loss.

A deed or mortgage in the chain of title may be a forgery.

A deed or a mortgage may have been signed by a person under age.

A deed or a mortgage may have been made by an insane person or one otherwise incompetent.

A deed or a mortgage may have been made under a power of attorney after its termination and would, therefore, be void.

A deed or a mortgage may have been made by a person other than the owner, but with the same name as the owner.

The testator of a will might have had a child born after the execution of the will, a fact that would entitle the child to claim his or her share of the property.

A deed or mortgage may have been procured by fraud or duress.

Title transferred by an heir may be subject to a federal estate tax lien.

An heir or other person presumed dead may appear and recover the property or an interest therein.

A judgment or levy upon which the title is dependent may be void or voidable on account of some defect in the proceeding.

Title insurance covers attorneys’ fees and court costs.

Title insurance helps speed negotiations when you’re ready to sell or obtain a loan.

By insuring the title, you can eliminate delays and technicalities when passing your title on to someone else.

Title insurance reimburses you for the amount of your covered losses.

A deed or mortgage may be voidable because it was signed while the grantor was in bankruptcy.

Each title insurance policy we write is paid up, in full, by the first premium for as long as you or your heirs own the property.

There may be a defect in the recording of a document upon which your title is dependent.

Claims constantly arise due to marital status and validity of divorces. Only title insurance protects against claims made by non-existent or divorced “wives” or “husbands.”

Many lawyers, in giving an opinion on a title, protect their clients as well as themselves, by procuring title insurance.

Over the last 24 years, claims have risen dramatically.

Dedicated to innovation and passionate about service, Title First Agency is your comprehensive, nationwide resource for title and real estate settlement services. Headquartered in Columbus, Ohio, Title First has branch offices throughout the Midwest and a robust virtual partner network throughout the country. Title First got its start in 1956 as an affiliate of a local law firm and has since emerged as one of the largest independent title agencies in the nation.

Proudly servicing Realtors, lenders, builders, developers, law firms, buyers and sellers, Title First is equipped to serve your residential and commercial title and settlement needs. Title First Agency. Your title company.

See Our National Coverage Map

See Our National Coverage Map