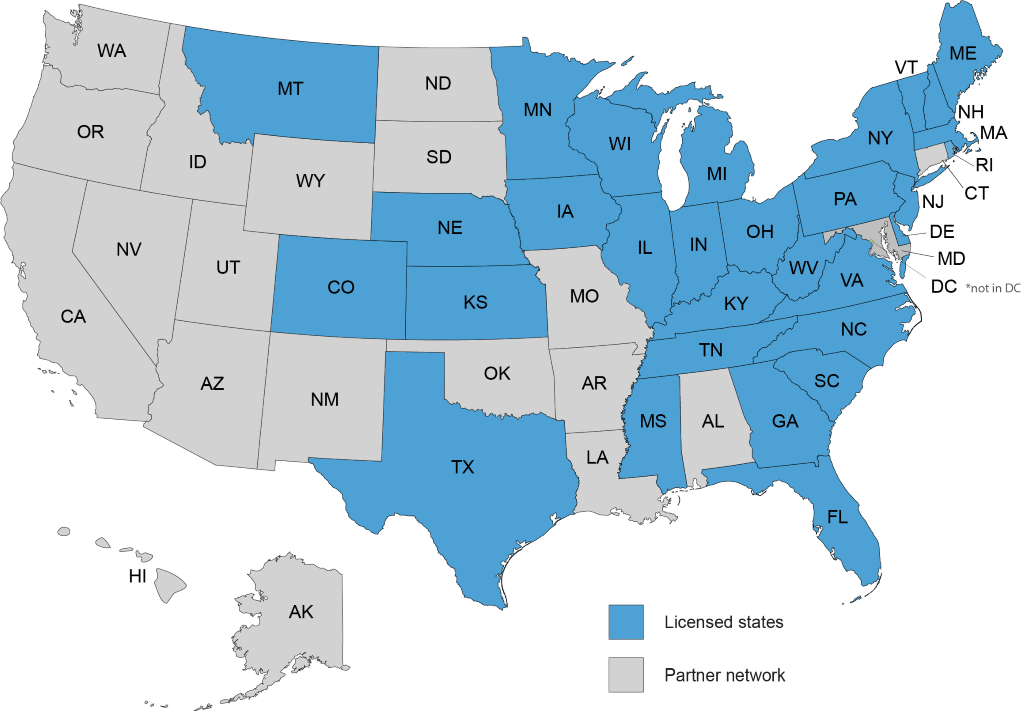

See Our National Coverage Map

See Our National Coverage Map

If you are planning on buying or selling a home, it’s important to understand that there can be delays in the closing. A real estate contract and the terms and conditions that are set forth in a contract do carry significant importance, but there can always be an issue.

In almost any real estate transaction that includes mortgage financing, the lender requires title insurance. The title company will conduct a search of the property’s title history to look for anything that might affect the buyer’s—and therefore the lender’s—interest in the property. Any defect in title raises the possibility of some third party asserting their own interest in the property. Liens, which give creditors a non-possessory interest in real property, are a common type of title defect. Before a closing may proceed, all title defects must be resolved to the satisfaction of the title insurance company.

If an appraisal comes back to a lender that values the home at less than the agreed-upon loan amount, it may hold up the process. Lenders will not approve loans for more money than a home is appraised for. Sellers might then lower the price of the home or choose to complete home repairs to increase the property’s value. Buyers could front the difference between the appraisal value and the original sale price. The parties could also contest the appraisal. Whichever the eventual solution, the closing date will likely move further into the future.

Home inspections can uncover mold problems, faulty wiring, roof leaks, fire hazards, code violations, cracks in the home’s foundation, and many other potential problems. Smaller issues can even put a closing on hold until the seller resolves the problem to the buyer’s satisfaction. The buyers may also discover a problem for themselves during the final walk-through of a home. They may observe problems with the plumbing, electrical, or HVAC systems, or notice that the sellers didn’t perform an agreed-upon repair or concession.

The Bottom Line: The process of buying or selling a home can be trying and a lot of the issues are simply out of your control. While these listed above are just the most common reasons a closing is delayed, there are plenty of smaller issues. It’s important to have a qualified and knowledgeable Realtor that can deal with last-minute issues and surprises and will stay on top of every step until you hear the magical words: “Clear to Close”.