1. Prepare your home for maximum earnings There are simple steps you can take to maximize your home’s appeal.

2. Enlist the help of a Realtor® to market and sell your home When selling your home, a Realtor® can provide expertise in valuing and advertising your home, qualifying and screening potential buyers, and negotiating contracts. If you are not able to enlist help from a Realtor®, Title First can provide you with assistance.

3. Negotiate a contract When you receive an offer for the purchase of your home, it must be in writing, generally on a preprinted real estate purchase contract from your local bar association or board of Realtors®. You may modify or alter the offer in any way you, your Realtor®, or your attorney wish. Offers and counter offers are made until the terms of the contract have been fully agreed to by all parties. When assessing offers and making counter-offers to the seller, don’t feel pressured to accept less than the value of your home.

4. Close on the property Before your home is officially sold, you must sign all appropriate documentation at your closing.

The closing will typically be held at a Title First office, the office of your realtor, lender or attorney, or sometimes on-location. Because your home represents one of the most significant investments you will make throughout your life, it is important that you feel comfortable with all the information being presented to you during the closing procedure.

Title First is dedicated to walking you through this important process with care and attention. When it’s time to set up your closing, don’t hesitate to tell your realtor or lender to call Title First, or feel free to give us a call if you’re working by yourself.

Be prepared for these seller’s fees commonly seen at the closing

Fees: Current loan payoff Conveyance fee, Title insurance examination, Title insurance commitment/premium for owner policy

Documentation to provide your Realtor® with: Tax receipts, Utility bills, Mortgage Payment

Information to provide to Title First: Your mortgage company name, address and account number. Any existing title insurance policy.

It can be a lot of work. But it can be done. Getting your house ready to sell in thirty days. The goals being available by the Spring 2019 Market, and getting top dollar. Expert Realtors will tell you that with motivation, hard work and focus it can be done.

Disconnect personally to your home. Invite a friend or family member over to look around to see what you do not. Fresh eyes can see where repairs are needed – it’s funny how a homeowner misses something simple that they see every day – and can be fixed easily.

Depersonalize rooms. Pack up photographs, family heirlooms, Buyers have a tough time seeing past the personal. They will need to imagine their own photos, art and other effects in the home without the distraction. It’s OK to leave a few framed photos around to make the home seem inviting and well lived in.

Declutter. Box up books from bookcases. Pack up knickknacks. Clean kitchen and bathroom counters. This can also mean removing extra pieces of furniture to be able to show the full potential of a room’s size.

Consider hiring someone to come in and make your home shine. Someone to clean beyond the usual day to day or weekly cleaning. Remember the first impression is the strongest. Dirty floors, dusty surfaces, and bad smells can ruin that first visit to your home. Empty out closets, drawers, under beds, and kitchen cabinets. Less makes everything appear more.

Paint the walls. Stick to whites, light grays, and light beiges that will make your home appear bigger, brighter and more welcoming. Adding a fresh coat of paint to your home will also help cover the wall’s imperfections and convey a blank slate to potential buyers.

Spruce up the exterior of the home, even consider hiring a landscaping company. Plenty of times, buyers pull up to a home only to back out because they don’t like the way the exterior looks. Get rid of dead plants, trim overgrown bushes and trees, freshen up the ground cover, add flowers that will survive the March temperatures for a punch of color. Adding new hardware to the front door or giving it a fresh coat of paint is a cheap thing to do and can speak volumes.

Thirty days is ample enough to get your home ready to sell. Find the best Realtor in your area and have them tell you what you will need to do to sell your home fast. The Spring and Summer selling market are typically the very best time to sell, but forewarning: there will be an increased inventory and the competition will be steep. Buyers will be pickier so you will need your home in it’s best shape as well as priced right.

Appraisal management company (AMC): An institution operated independently of a lender that, once notified by a lender, orders a home appraisal. Appraisal: An informed, impartial and well-documented opinion of the value of a home, prepared by a licensed and certifed appraiser and based on data about comparable homes in the area as well as the appraiser’s own walk-through. Approved for short sale: A term that indicates that a homeowner’s bank has approved a reduced list price on a home and the home is ready for resale. American Society of Home Inspectors (ASHI): A not-for-profit professional association that sets and promotes standards for property inspections and provides educational opportunities to its members. (i.e., Look for this accreditation or something similar when shopping for a home inspector.)

Attorney state: A state in which a real estate attorney is responsible for closing. Back-end ratio: One of two debt-to-income ratios that a lender analyzes to determine a borrower’s eligibility for a home loan. The ratio compares the borrower’s monthly debt payments (proposed housing expenses, plus student loan, car payment, credit card debt, maintenance or child support and installment loans) to gross income. Buyer’s market: Market conditions that exist when homes for sale outnumber buyers. Homes sit on the market a long time and prices drop. Meaning = you win. Cancellation of escrow: A situation in which a buyer backs out of a home purchase. Capacity: The amount of money a home buyer can afford to borrow. Cash-value policy: A homeowners insurance policy that pays the replacement cost of a home, minus depreciation, should damage occur. Closing: A meeting during which ownership of a home is transferred from seller to buyer. The closing is usually attended by the buyer, the seller, both real estate agents and the lender. Closing costs: Fees associated with the purchase of a home that are due at the end of the sales transaction. Fees may include the appraisal, the home inspection, a title search, a pest inspection and more. Buyers should budget for an amount that is 1 to 3 percent of the home’s purchase price. Closing Disclosure (CD): A five-page document sent to the buyer three days before closing. This document spells out all the terms of the loan: the amount, the interest rate, the monthly payment, mortgage insurance, the monthly escrow amount and all closing costs. Closing escrow: The final and official transfer of property from seller to buyer and delivery of appropriate paperwork to each party. Closing of escrow is the responsibility of the escrow agent. Comparative Market Analysis (CMA): An in-depth analysis, prepared by a real estate agent, that determines the estimated value of a home based on recently sold homes of similar condition, size, features and age that are located in the same area. Compliance agreement: A document signed by the buyer at closing, in which he or she agrees to cooperate if the lender needs to fix any mistakes in the loan documents. Comps: Or comparable sales, are homes in a given area that have sold within the past six months that a real estate agent uses to determine a home’s value. Condo insurance: Homeowners insurance that covers personal property and the interior of a condo unit should damage occur. Contingencies: Conditions written into a home purchase contract that protects the buyer should any issues arise with financing, the home inspection or other. Conventional 97: A home loan that requires a down payment equivalent to 3 percent of the home’s purchase price. Private mortgage insurance, which is required, can be canceled when the owner reaches 80 percent equity. Conventional loan: A home loan not guaranteed by a government agency, such as FHA or the VA. Days On Market (DOM): The number of days a property listing is considered active. Depository institutions: Banks, savings and loans and credit unions. These institutions underwrite as well as set home loan pricing in-house. Down payment: A certain portion of the home’s purchase price that a buyer must pay. A minimum requirement is often dictated by the loan type. Debt-to-income ratio (DTI): A ratio that compares a home buyer’s expenses to gross income. Earnest money: A “security deposit” made by the buyer to assure the seller of his or her intent to purchase. Equity: A percentage of the home’s value owned by the homeowner. Escrow account: An account required by a lender and funded by a buyer’s mortgage payment to pay the buyer’s homeowners insurance and property taxes. Escrow agent: A neutral third-party officer who holds all paperwork and funding in trust until all parties in the transaction fulfill their obligations as part of the transfer of property ownership. Escrow state: A state in which an escrow agent is responsible for closing. Fannie Mae: A government-sponsored enterprise chartered in 1938 to help ensure a reliable and affordable supply of mortgage funds throughout the country. Federal Reserve: The central bank of the United States, established in 1913 to provide the nation with a safer, more flexible and more stable monetary and financial system. Federal Housing Administration (FHA): A government agency created by the National Housing Act of 1934 that insures loans made by private lenders. FHA 203(k): A rehabilitation loan backed by the federal government that permits home buyers to finance money into a mortgage to repair, improve or upgrade a home. Foreclosure: A property repossessed by a bank when the owner fails to make mortgage payments. Freddie Mac: A government agency chartered by Congress in 1970 to provide a constant source of mortgage funding for the nation’s housing markets. Funding fee: A fee that protects the lender from loss and also funds the loan program itself. Examples include the VA Funding Fee and the FHA funding fee. Gentrification: The process of rehabilitation and renewal that occurs in an urban area as the demographic changes. Rents and property values increase, culture changes and lower-income residents are often displaced. Guaranteed replacement coverage: Homeowners insurance that covers what it would cost to replace property based on today’s prices, not the original purchase price, should damage occur. Homeowner Association (HOA): The governing body of a housing development, condo or townhome complex that sets rules and regulations and charges dues and special assessments that are used to maintain common areas and cover unexpected expenses respectively. Home equity line of credit (HELOC): A revolving line of credit with an adjustable interest rate. Like a credit card, this line of credit has a limit. There is a specified time during which money can be drawn; payment in full is due at the end of the draw period. Home equity loan: A lump-sum loan that allows the homeowner to use the equity in his or her home as collateral. The loan places a lien against the property and reduces home equity. Home inspection: A non-destructive visual look at the systems in a building. Inspection occurs when the home is under contract or in escrow. Homeowners insurance: A policy that protects the structure of the home, its contents, injury to others and living expenses should damage occur. Housing ratio: One of two debt-to-income ratios that a lender analyzes to determine a borrower’s eligibility for a home loan. The ratio compares total housing cost (principal, homeowners insurance, taxes and private mortgage insurance) to gross income. In escrow: A period of time (30 days or longer) after a buyer has made an offer on a home and a seller has accepted. During this time, the home is inspected and appraised and the title searched for liens, etc. Jumbo loan: A loan amount that exceeds the Fannie Mae/Freddie Mac limit, which is generally $425,100 in most parts of the United States. List price: The price of a home, as set by the seller. Loan estimate: A three-page document that is sent to an applicant three days after he or she applies for a home loan. The document includes loan terms, monthly payment and closing costs. Loan-to-value ratio (LTV): The amount of the loan divided by the price of the house. Lenders reward lower LTV ratios. Market value coverage: Homeowners insurance that covers the amount the home would go for on the market, not the cost to repair, should damage occur. Mechanic’s lien: A hold against a property, filed in the county recorder’s office by someone who’s done work on a home and not been paid. If the homeowner refuses to pay, the lien allows a foreclosure action. Mortgage broker: A licensed professional who works on behalf of the buyer to secure financing through a bank or other lending institution. Mortgage companies: Lenders who underwrite loans in-house and fund loans from a line of credit before selling them off to a loan buyer. Mortgage interest deduction: Mortgage interest paid in a year subtracted from annual gross salary. Mortgage interest rate: The price of borrowing money. The base rate is set by the Federal Reserve and then customized per borrower, based on credit score, down payment, property type and points the buyer pays to lower the rate. Multiple Listing Service (MSL): A database where real estate agents list properties for sale. Origination fee: A fee, charged by a broker or lender, to initiate and complete the home loan application process. Piggyback loan: A combination of loans bundled so as to avoid private mortgage Insurance. One loan covers 80 percent of the home’s value, another loan covers 10 to 15 percent of the home’s value and the buyer contributes the remainder. Principal, interest, property taxes and homeowners insurance (PITI): The components of a monthly mortgage payment. Private mortgage insurance (PMI): A fee charged to borrowers who make a down payment that is less than 20 percent of the home’s value. The fee, 0.3 percent to 1.5 percent of the yearly loan amount, can be canceled, in certain circumstances, when the borrower reaches 20 percent equity. Points: Prepaid interest owed at closing, with one point representing one percent of the loan. Paying points, which are tax deductible, will lower the monthly mortgage payment. Pre-approval: A thorough assessment of a borrower’s income, assets and other data to determine a loan amount he or she would qualify for. A real estate agent will request a pre-approval or pre-qualification letter before showing a buyer a home. Pre-qualification: A basic assessment of income, assets and credit score to determine what, if any, loan programs a borrower might qualify for. A real estate agent will request a pre-approval or pre-qualification letter before showing a buyer a home. Property tax exemption: A reduction in taxes based on specific criteria, such as installation of a renewable energy system or rehabilitation of a historic home. Round table closing: All parties (the buyer, the seller, the real estate agents and maybe the lender) meet at a specified time to sign paperwork, pay fees and finalize the transfer of homeownership. Seller’s market: Market conditions that exist when buyers outnumber homes for sale. Bidding wars are common. Short sale: The sale of a home by an owner who owes more on the home than it’s worth (i.e. “under water” or “upside down”). The owner’s bank must approve a lower list price before the home can be sold. Special assessment: A fee charged by a condo complex HOA when cash on reserve is not enough to cover unexpected expenses. Tax lien: The government’s legal claim against property when the homeowner neglects or fails to pay a tax debt. Third-party review required: Verbiage included in a home listing to indicate that the lender has not yet approved the home for short sale. The seller must submit the buyer’s offer to the lender for approval. Title insurance: Insurance that protects the buyer and lender should an individual or entity step forward with a claim that was attached to the property before the seller transferred legal ownership of the property or “title” to the buyer. Transfer stamps: The form in which transfer taxes are paid by the home buyer. Stamps can also serve as proof of transfer tax payment. Transfer taxes: Fees imposed by the state, county or municipality on transfer of title. Under contract: A period of time (30 days or longer) after a buyer has made an offer on a home and a seller has accepted. During this time, the home is inspected and appraised and the title searched for liens, etc. Under water or upside down: A situation in which a homeowner owes more for a property than it’s worth. Underwriting: A process a lender follows to assess a home loan applicant’s income, assets, credit etc. and the risk involved in offering the applicant a mortgage. VA home loan: A home loan partially guaranteed by the United States Department of Veteran Affairs and offered by private lenders, such as banks and mortgage companies. VantageScore: A credit scoring model relied upon by lenders to make lending decisions. A borrower’s score is based on bill-paying habits, debt balances, age and variety of credit accounts and number of inquiries on credit repots. Walk-through: A buyer’s final inspection of a home before closing. Water certificate: A document that certifies that a water account has been paid in full. The seller must produce this certificate at closing.

A fire destroys only the house and improvements. The ground is left. A defective title may take away not the only the house but also the land on which it stands. Title insurance protects you (as specified in the policy) against such loss.

A deed or mortgage in the chain of title may be a forgery.

A deed or a mortgage may have been signed by a person under age.

A deed or a mortgage may have been made by an insane person or one otherwise incompetent.

A deed or a mortgage may have been made under a power of attorney after its termination and would, therefore, be void.

A deed or a mortgage may have been made by a person other than the owner, but with the same name as the owner.

The testator of a will might have had a child born after the execution of the will, a fact that would entitle the child to claim his or her share of the property.

A deed or mortgage may have been procured by fraud or duress.

Title transferred by an heir may be subject to a federal estate tax lien.

An heir or other person presumed dead may appear and recover the property or an interest therein.

A judgment or levy upon which the title is dependent may be void or voidable on account of some defect in the proceeding.

Title insurance covers attorneys’ fees and court costs.

Title insurance helps speed negotiations when you’re ready to sell or obtain a loan.

By insuring the title, you can eliminate delays and technicalities when passing your title on to someone else.

Title insurance reimburses you for the amount of your covered losses.

A deed or mortgage may be voidable because it was signed while the grantor was in bankruptcy.

Each title insurance policy we write is paid up, in full, by the first premium for as long as you or your heirs own the property.

There may be a defect in the recording of a document upon which your title is dependent.

Claims constantly arise due to marital status and validity of divorces. Only title insurance protects against claims made by non-existent or divorced “wives” or “husbands.”

Many lawyers, in giving an opinion on a title, protect their clients as well as themselves, by procuring title insurance.

Over the last 24 years, claims have risen dramatically.

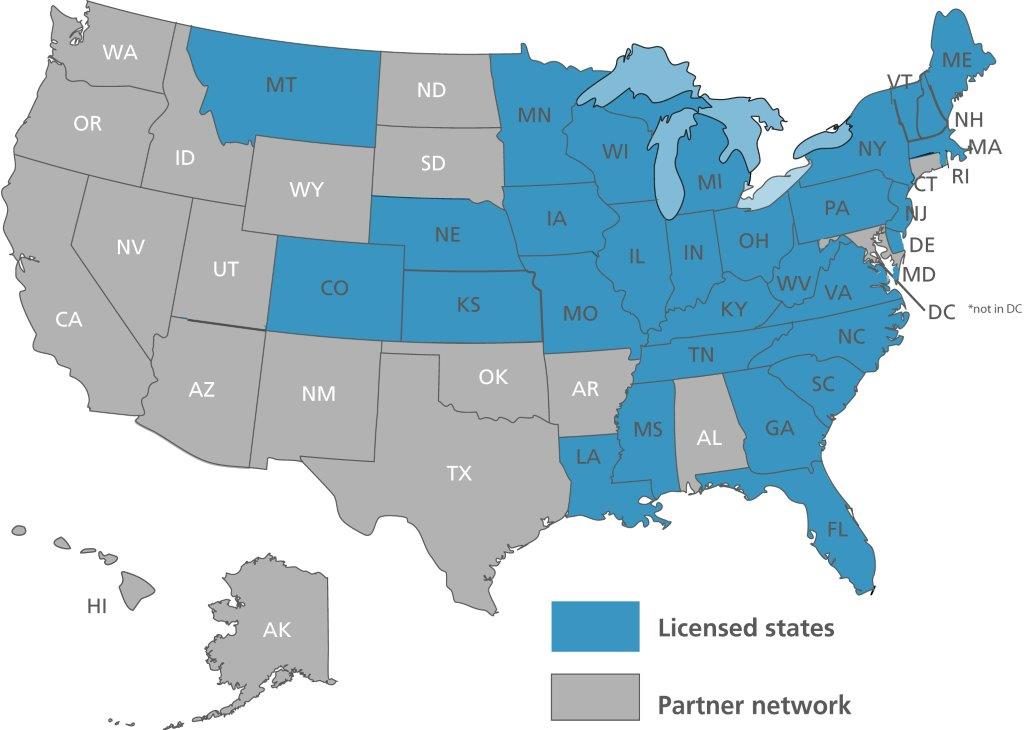

Dedicated to innovation and passionate about service, Title First Agency is your comprehensive, nationwide resource for title and real estate settlement services. Headquartered in Columbus, Ohio, Title First has branch offices throughout the Midwest and a robust virtual partner network throughout the country. Title First got its start in 1956 as an affiliate of a local law firm and has since emerged as one of the largest independent title agencies in the nation.

Proudly servicing Realtors, lenders, builders, developers, law firms, buyers and sellers, Title First is equipped to serve your residential and commercial title and settlement needs. Title First Agency. Your title company.

Spring is right around the corner and while we are in the cold, gray days of February, now is a perfect time to get your home ready to put on the market to sell during the Spring market!

Start purging and packing. Go through your closets, attic, garage, basement, junk drawers and decide what you can throw out and what you want to save but don’t need and can box up. Reducing the amount of clutter will help potential buyers visualize how they might use the different areas. Plus, the less you have in a closet – the bigger it will seem.

Make improvements especially in the kitchen and bathrooms. It doesn’t need to be expensive. For instance, how do your kitchen cabinets look? Are they chipped or are the knobs falling off? Replace or repaint them, tighten the knobs or replace the hardware completely. Regrout tile where needed, caulk the shower and tub, replace switch plates and doorknobs- all this will give the bathroom a fresh look without breaking the bank.

How is your front door? The front hallway? The first thing a potential buyer will see when they come to your home. Give it a fresh coat of paint and clean or replace the knob and knocker if there is one. Look around at the foyer area and notice if you need to update the walls with neutral paint or clean the trim, if any.

Use neutral, gray or white paint on the walls in each room. Another relatively cheap and easy thing to do in the Winter months to get ready for Spring. Don’t just touch up – paint the entire wall. Now is the time to paint over the bright colors you may have used. If you have carpeting in any room, consider replacing to hardwood which will help the home sell, or at the very least get a good professional cleaning.

Go room to room in your warm home while the February snow is falling outside and scrutinize everything from switch plates to ceiling fans. Look for the tiny flaws that you haven’t noticed like cob webs in between the storm & the window. Have you dusted the shades? Cleaned the curtains? Not something people think to do on the weekly, but can make a huge difference. Simply get on the floor at kid and dog level and wipe down the baseboards and look for little fingerprints to wash away with mild soap and water. Put the brush attachement on your vacuum and run it over the walls.

The Bottom Line: It’s surprising, the little things you don’t notice daily in your home. But, taking the time and seeing things through the eyes of a potential buyer can greatly help to get your home ready for Spring. Sometimes asking a friend to come to do an honest walk through and point out problems will help. Now, might also be the perfect time to find a Realtor and have them come in your home and give you their feedback as well.

With wire fraud and email hacking on the rise, we must all become more diligent in protecting our clients’ information. At Title First Agency, we take security seriously and we put our company through a rigorous audit (SSAE 18). In December, we had a perfect report for the 4th year in a row. This is one of the steps we take to make sure our clients’ data is safe and secure. Title First is one of only a handful of title agencies across the country to go through these audits

Another aspect of protecting our clients’ information is educating prospective buyers, sellers and real estate professionals about the dangers of wire fraud and email hacking. While buying and selling a home is an exciting time, there can be pitfalls for unsuspecting consumers. We’ve made a video with four tips to protect money and advice on what to do if targeted by a scam.

Title First Agency’s software platform and third-party integrations are crucial to providing our clients with the most efficient title services. Our objective is to continually refine state of the art technology to assist with compliance. This is achieved by working with the top technology providers in the business. We also work closely with residential realtors and their clients, through the escrow and title process to make sure that proper steps are taken to successfully close.

The Bottom Line: Protecting against wire fraud and email hacking requires all parties of a transaction to stay diligent throughout the process. If there are any questions regarding potential wire fraud, email hacking or anything else that feels “off”, Title First Agency is here to be contacted to discuss any issue with our agents.

A real estate appraisal is an essential piece of the buying and selling of property most notably if a buyer is going to need a loan to buy the home. No legitimate financial institution will lend money without an appraisal. The appraisal value of a home can make or break a sale, leaving this part of the real estate process one if not the most important, critical steps.

A home appraisal is different from a home inspection even though both an appraiser and an inspector will walk inside, outside and around the property to check everything with a fine tooth comb. The appraiser is finding the value of the home and the inspector is looking for problems or defects with it.

During an appraisal of a home, the appraiser will look at the state of repari, the features, square footage, number of bedrooms and bathrooms. It is good to give a list of repairs and improvements made such as a new roof, water heater, air conditioning, etc. Basically, anything the owner of the home can think of that will help the appraiser decide the general market value of the home.

The home will then be compared as accurately as possible by way of recent sales, homes sold that are similar, and a search will be done for properties that are identical to yours and what’s been sold or what is on sale in the neighborhood. The appraiser will also provide whether values of home are on the rise, decreasing or stable. If there are any concerns that he feels will harm the property’ value, it will be noted as well as flagging any bigger problems he may see in the foundation, the roof or any noticeable water leaks in ceilings or floors.

Again, an appraisal can make or break a sale of the home so it’s a nerve-wracking time. If the appraisal comes back higher or lower than the sale price, there will need to be more negotiating. If the seller isn’t happy with the outcome, a good Realtor will discuss with the appraiser why certain decisions were made. With the help of a Realtor, the seller can put together a valid argument as to why the appraisal is not correct.

Appraisals are valid for six months unless the home is in certain markets where homes are selling fast and prices continually change. At which point, lenders usually like an appraisal every three months.

The Bottom Line: Any good Realtor will press on the point that pricing the home correctly is most important. If a home is overpriced it’s not going to appraise and the sale usually falls through. Pricing issues are the number one reason homes don’t sell.

Unfortunately, many people assume incorrectly that homes do not sell in the winter. Spring wins as people believe it is the best time to sell, but a good realtor will tell a seller that putting their home on the market in January to beat the competition. After the holidays, people are back at work and looking online for their next move, and with the mindset of so many sellers to wait until Spring, the home on the market in January will have less competition.

Real Estate becomes flooded come spring and summer and is dominated by high supply and high demand, meaning a home becomes one of the many for sale. Think about selling in a period of high demand but low supply, and being one of the few and standing out from the crowd and with less risk of getting lost in a market overload in the Spring.

Redfin, a real estate organization, took a look a home sales from 2010 through 2014 to determine how well homes sold based on the season. The findings were surprising for many people, because they went against the standard assumption that winter was a time to avoid trying to sell a home. They found that, indeed, homes did sell best in spring, but only by a small margin. The next best time to sell a home turned out to be winter, followed by summer and then fall. Winter home sales were only one percentage point lower than the figures for spring, with summer trailing quite a bit behind.

The buyers are more serious in the cold, dark months of January and February. It’s not so hard to go house hunting in the beautiful months in Spring and Summer, but to go out in the frigid temps to look at homes means that buyer is motivated.

January is the most popular month for corporate transfers. People who are transferring for work are highly motivated buyers and are limited to the time they can spend looking for a house. Take advantage of this situation, especially if living in an area with corporate headquarters, or major employers.

Buying a home can be chock full of complications and setbacks, or it can go remarkably smooth and fast if it is planned carefully. The Realtor needs to stay focused and be the voice of reason as they facilitate the process at closing and make sure all parties have completed all unfinished business prior to coming to the “closing table”. Here’s a quick list that Realtors can use to ensure a smooth closing.

Repairs: The Realtor should check on the status of all repairs that were to be made on the home the day before closing. If there was an agreement that something needed to be fixed by closing, make sure that it is. If there was an arrangement for repairs to be taken care of after closing, make sure all the necessary paperwork shows this as fact. A final walk-through should be done with the buyers. The sellers should make sure, with their Realtor, that the property is in the condition promised and all of their personal items are removed.

Title Insurance: All of the title work should be checked to ensure clear title and that the property can be transferred without any obstructions. Should there be any title issues that might include judgments or liens, they must be settled prior to the hour of closing. The moment of truth in a real estate transaction happens at the closing table. Title First Agency will work hard to ensure a seamless experience for you and your clients. From contract to closing, we handle all the details to help a transaction run smoothly and close on time.

Financing: The lender should be contacted the day before the closing to be certain that all the documents they need have been received. Occasionally, the closing is delayed due to one document or one final verification. The interest rate for the loan should be locked as well as the final mortgage and monthly payments. The Realtor should make sure the buyer has all the funds available and ready to close. Having everything in hand the day before gives both the buyer and the seller 24 hours to review everything and have any questions ready, errors noticed or points not understood addressed.

The Bottom Line: A thorough Realtor will make sure the buyers are ready for the closing. First-time buyers may not realize all the people that could possibly be at the closing table, and all the paperwork there will be that needs their signature. The buyer needs a cashier’s check or arrangments made to wire the closing funds to the escrow company. The seller should bring all the keys, garage door openers, alarm codes and any other controls to the settlement. The Realtor should make sure and confirm that all utilities have been disconnected by the sellers and set up ready for the buyers upon closing.

Are the walls closing in on you in your home? Are you feeling cramped? Maybe you have TOO much space and have launched all of your children and are ready to downsize. Are you ready to find your next home? Are you on the fence whether it’s a good time to sell or not? Of course, you want top dollar. So what are some of the signals that now is the time – or not?

Positive Equity: The current market value of your home, less what you owe. If you can sell your home for more than you owe, you will benefit from positive equity. This can enable you to have enough money for closing costs and putting money down on your next home. At the very least, you want to be able to sell enough to cover the current balance of your mortgage. If none of this applies to you, there are many things you can do to improve the equity of your home, including home improvements. Speak with a skilled Realtor to know what you should repair, replace or upgrade.

Strong Market: You probably have a general idea of what is going on in your neighborhood – what the trend is; who is selling; what has sold and for how much. But, call your local Realtor and get the comps and find out exactly how hot the market is. You’ll be able to learn how long a home was on the market until it sold, what the price per square foot has been and if that number been increasing or decreasing. If it’s been low average days on market, it’s a pretty positive sign the market is hot for sellers.

Remodeling Won’t Raise The Value: Sometimes it’s beneficial to make updates in your home and you know that updating your kitchen or adding another bathroom will help you sell your home for top dollar. But, making an appointment with a reputable Realtor to find out if adding money to your home will be worth it. Depending on the real estate in your neighborhood and what buyers are looking for, doing less may be more. Your Realtor will help you to understand what the market is doing – the rule of thumb is not to raise your home’s value any higher than 10 percent of the average cost of homes in your neighborhood.

The Bottom Line: Is it finally time to sell? There are many signs, we’ve just listed three. Talk to a Realtor, meet with a financial advisor or mortgage lender and make sure it makes sense financially. Being house poor is a reality, and as much as you want a larger home – or even a smaller home – it might not be the right time for you.

See Our National Coverage Map

See Our National Coverage Map